[ad_1]

BUENOS AIRES (Reuters) – Argentine bond prices fell to record lows on Monday and the official and black market pesos diverged after the country imposed capital controls in a bid to stem a currency rout that is sharpening the risk of default.

The move on Sunday by President Mauricio Macri a free-markets advocate who abolished capital controls after he came to power in 2015, was a sharp about-face for his administration after the conservative leader was pummeled in primary elections in August.

The country’s peso, bonds and equities have since tumbled, forcing Macri to unveil plans to delay payments on around $100 billion of debts as well as the currency controls restricting the purchase of dollars.

The peso ARS=RASL closed 0.88% stronger in official markets, but closed 0.79% weaker in the black market at 63.5 per dollar, a divergence underscoring a loss of trust in the official price that was also helped by a market holiday in the United States.

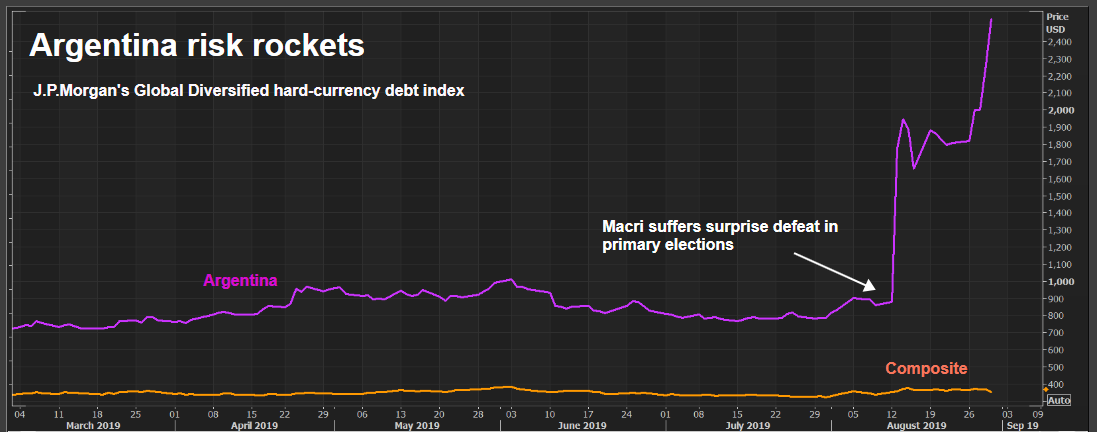

(For a graphic on Argentina risk, click here)

{kind=link}

(For a graphic on currency control, click here)

{kind=link}

“The dollar at this level is now strong enough,” Treasury Minister Hernan Lacunza told a news conference. “All these measures have the central objective of stability.”

The official peso had lost more than 23% since the Aug. 11 primary election turned the country’s politics on its head, with incumbent Macri getting soundly thrashed by his populist-leaning opponent Alberto Fernandez.

The currency is down more than a third so far this year, following a more than 50% drop last year. The central bank has burned through nearly $1 billion in reserves since Wednesday, but has failed to stem the peso’s slide.

Fernandez is now the clear front-runner ahead of the Oct. 27 general election. His vice presidential running mate is former President Cristina Fernandez de Kirchner, a free-spending populist who applied heavy-handed trade and currency controls during her two terms from 2007-2015.

The presence of Fernandez de Kirchner on the ticket has caused concern about the return of the interventionist left to power, although the more moderate Alberto Fernandez has said that he alone will set policy in his administration.

LONG LINES AT BANKS

Confidence is nonetheless running low. Unusually long lines formed at banks in Buenos Aires on Monday, with depositors looking to withdraw dollars or pesos from their account, despite the government saying the financial system remains solid.

“All these people are taking out what they have, or part of what they have, because they’d rather keep their cash at home at this stage,” 61-year-old depositor Julio Novoa told Reuters.

Having announced changes to Argentina’s bond payment scheduled last week, the application of currency controls was the second measure by Macri that flew in the face of his own promise to use orthodox policies to straighten out the chronically troubled economy. Macri’s new controls may be difficult to back out of later, analysts said.

“The problem with restrictive, emergency measures is that they are easier to apply than to retract,” said Buenos Aires-based financial analyst Christian Buteler in a tweet.

More peso weakness was expected ahead. “The game has changed for the foreign exchange market,” said Sabrina Corujo, an analyst with Buenos Aires brokerage Portfolio Personal, warning that local stocks and bonds were set to weaken as well.

The central bank has been authorized to restrict purchases of dollars as it burns through its reserves to prop up the peso. Investors fretted that once the controls are in place, they will be difficult to end, possibly leaving Argentina with an economy once again distorted by government intervention.

The reintroduction of controls was a sharp turnaround for Macri, a free-trade advocate who won the presidency in 2015 on promises of “normalizing” Latin America’s No. 3 economy by ditching the controls favored by the previous administration.

Argentina’s benchmark international 2028 dollar bonds 040114HQ6= dropped more than 2 cents to a new low of 36.5 cents, according to Refinitiv data. Bonds maturing in 2038 040114GK0= recorded similar losses.

Argentina’s euro-denominated sovereign bonds also suffered hefty losses to hit record lows on Monday. The 2022 bond AR150316022= dropped more than 10 cents to 34.45 cents while the 2027 issue AR150316049= tumbled 7.2 cents to 33.501 cents, according to Refinitiv data.

American depository receipts (ADRs) of Argentina’s financial institutions also came under pressure. Grupo Financiero Galicia’s Frankfurt-listing (GGAL.BA) (GGALyb.F) tumbled 9.15% while Banco Macro SA (BMA.BA) (BSUy.F) fell 6.5%.

Monday was an official holiday in the United States, which could help control losses in Argentine asset prices by reducing trading volumes, Buteler tweeted.

The risk premiums demanded by investors to hold Argentina’s dollar bonds .JPMEGDARGR over safe-haven U.S. Treasuries rocketed to 2,534 basis points on J.P. Morgan’s index of hard-currency emerging market bonds .JPMEGR – levels last seen in the wake of a major 2001 default.

“(Capital controls are) a sign of distress in the market and reflect that the new parameters on Argentina are weak and when the peso weakens further it weighs on the credit profile,” said Michael Bolliger, head of asset allocation for emerging markets at UBS Wealth Management.

“There remains a lot of pressure on the currency … There’s a limit to what they can do without capital controls.”

Reporting by Karin Strohecker, Eliana Raszewski, Walter Bianchi, Marina Lammertyn and Hugh Bronstein; Additional reporting by Tom Arnold and Marc Jones; Editing by Steve Orlofsky, Nick Zieminski and Peter Cooney

[ad_2]

Source link